An IPO can expose weak close processes before the registration statement is ready. For a middle-market CFO, undocumented controls and late audit adjustments can turn a planned filing into a costly delay.

Ready to prepare for your IPO? Contact GuzmanGray for audit, controls, tax, and assurance support.

The immediate question is not whether the company wants an IPO, but whether its records, controls, people, and advisers can support one under scrutiny. IPO readiness audit checklist: What CFOs need to prove sets the evidence standard for a credible filing plan. Here’s how.

IPO readiness audit checklist: What CFOs need to prove

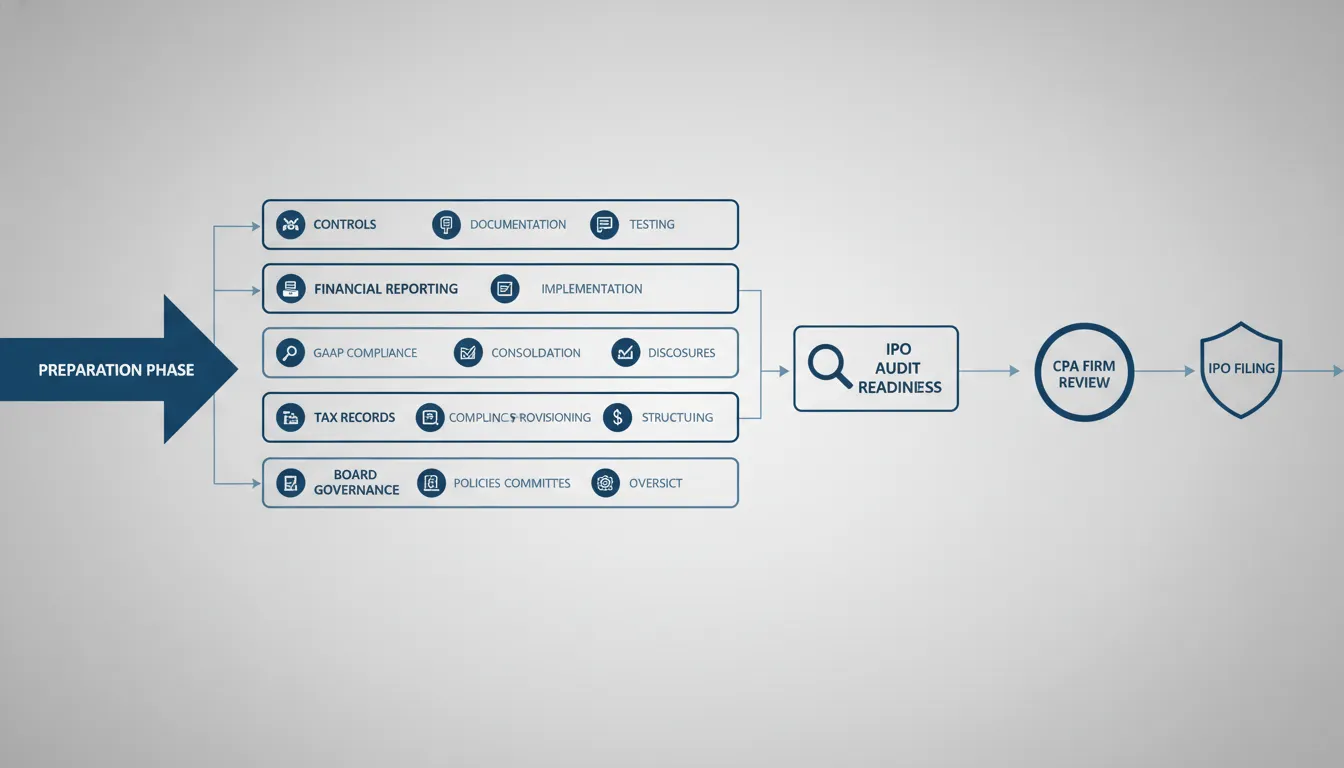

An IPO readiness audit checklist helps a CFO test whether the business can meet public-company demands before filing begins. It should map financial statements, close quality, accounting policies, controls, SEC reporting capacity, tax positions, governance, systems, and adviser responsibilities.

Audit-ready financial records

An IPO readiness audit checklist starts with evidence, not a planned filing date. CFOs need financial statements that can stand up to public review. They also need close records, accounting policies, reconciliations, and support for key judgments. These records let auditors trace amounts to sound source data.

A readiness review asks if prior periods are consistent and complex transactions are recorded correctly. It tests whether audit requests can be answered on time. It also tests whether the company has the people and systems needed after listing. GuzmanGray is a PCAOB-registered audit firm, which matters when the path leads to public-company audits.

Reporting and control evidence

A public company reports under a different level of review. The SEC states that public companies face annual, quarterly, and current reporting duties. Its IPO building blocks guidance also points companies toward reliable accounting controls and record-keeping systems. CFOs should prepare evidence for both reporting and control design.

A CPA-led checklist goes beyond a list of filings. It asks who owns each close task and what review proves it was done. It also asks where errors could affect disclosure. Scope should include revenue, equity, debt, related parties, estimates, consolidation, and data used in reports.

- Document the monthly and quarter-end close, with review evidence and issue tracking.

- Map major accounts and disclosures to controls, owners, supporting files, and testing plans.

- List open accounting matters and set dates for management and auditor decisions.

- Confirm reporting data can be gathered, reviewed, and explained without late manual fixes.

Tax and advisor readiness

Tax readiness belongs in the same work plan as audit readiness. CFOs should assemble returns, provision workpapers, entity charts, tax attributes, uncertain tax positions, and state filing support. Gaps can slow diligence. They can also lead to late changes or make public reports harder to support.

The CFO should also show that the advisor team can work from one clear fact set. Auditors, tax advisors, securities counsel, bankers, and management need set timelines and responsibility lists. Legal and software checklists can track actions. A CPA firm tests whether financial evidence, controls, and tax support are ready for review.

Audit and financial reporting checklist before an IPO

Before an IPO, CFOs need audit-ready support for each material number, disclosure, and judgment. The checklist should confirm source records, review evidence, accounting policies, reporting owners, and the timing needed to answer auditor and SEC questions without late manual fixes.

An IPO readiness audit checklist begins with one question: can the finance team support each reported number with clear evidence? Public company scrutiny tests more than totals. It tests review steps, source records, timing, and ownership of each filing input.

The SEC advises companies preparing for public life to assess accounting controls, reporting systems, and records for timely disclosure. CFOs can use this SEC IPO preparation guidance as a baseline for finance work.

Historical financial statement file

Start with the historical periods expected in the offering process. Build one indexed file for audited statements, trial balances, ledgers, reconciliations, debt schedules, equity records, tax support, and material contracts. Tie each schedule to the general ledger and record who reviewed it.

Keep a separate log for changes to close entries, accounting policies, estimates, and unusual deals. A clean log lets the auditor trace a balance without chasing emails. It also helps management explain adjustments in disclosure drafts and due diligence sessions.

Readiness file comparison

| Readiness area | IPO-ready file |

|---|---|

| Monthly close | Close calendar and reconciliations. |

| Audit support | Indexed evidence with ledger ties. |

| Policies | Written GAAP policies and approvals. |

| Disclosures | Owners, checklists, and support files. |

| Independence | Service review and approval record. |

Use the file as a dry run before the audit cycle starts. Ask each owner to produce support from the index, not a personal inbox. Log missing records, late reviews, and policy gaps. Then assign fixes with due dates. This test shows whether reporting works under pressure.

Close control and auditor independence

GAAP close discipline is practical. Set a monthly close calendar, assign account owners, require review evidence, and track unresolved items. Run the process on a public-company timetable before filing pressure begins. Missed handoffs will surface while the team can still fix them.

Discuss independence early with the audit firm and the board or audit committee. List current and planned services, related relationships, fees, and approvals in one record. If the company needs a public-company audit, confirm the firm’s relevant standing and experience. GuzmanGray describes its public-company audit services for this work.

Disclosure-ready evidence room

A CFO should make disclosures easy to verify. Create folders for business operations, financial condition, management information, risks, related parties, equity, debt, commitments, and subsequent events. Name an owner for each folder, then mark review status and open questions.

The evidence room should map each draft disclosure back to source support. The SEC notes that public company reports generally include business operations, financial condition, and management information. A documented map supports the required reporting scope and reduces last-minute searches.

- Maintain one request list with owner, due date, reviewer, and final evidence link.

- Archive audit adjustments, management conclusions, and approval records in the same index.

- Test the file by asking a reviewer to trace selected disclosures from draft to source.

This preparation does not remove audit questions. It gives the finance team a controlled way to answer them, update drafts, and show how each decision was made.

How do controls, governance, and SOX readiness fit in?

Controls, governance, and SOX readiness turn IPO preparation into a repeatable reporting process. CFOs should identify control owners, document review steps, test high-risk areas, brief the audit committee, and remediate gaps before filing pressure compresses the timeline.

Controls that support public reporting

An IPO readiness audit checklist should test whether financial reporting can hold up under public-company demands. The SEC asks IPO candidates to consider the reliability of accounting controls, procedures, reporting, and record-keeping systems. These systems help support timely and accurate disclosure. The SEC’s IPO building blocks make controls a core part of preparation, not a late-stage cleanup item.

Start with internal controls over financial reporting, often called ICFR. Map each material account and disclosure to its key risks, controls, owners, evidence, and review steps. The map should cover close activities, revenue, journal entries, estimates, access to systems, and financial statement review. If a control cannot be shown with dated evidence, it is not ready for audit testing.

Ownership, oversight, and segregation of duties

Segregation of duties is often hard in a lean finance team. No one person should prepare, approve, post, and reconcile the same material transaction. Where staffing limits that split, document a review control by a qualified leader. Track system access, approval limits, and exceptions in one control inventory, then test that practice matches the written design.

Governance readiness runs in parallel. Management should set a reporting calendar, assign disclosure owners, and prepare clear updates for the board and audit committee. The audit committee needs time to review financial reporting risks, auditor communications, and remediation status. Choosing a internal control audit firm also aligns the audit conversation with public-company requirements.

Board materials should match the control story management can prove. Include close results, critical estimates, control findings, open fixes, and any needed resources. That view helps directors ask focused questions before a registration process places more pressure on reporting deadlines.

SOX scoping and practical milestones

SOX readiness becomes manageable when it is scoped from the financial statements back to risk. Begin with material accounts, key disclosures, major locations, and systems that feed the close. Then identify entity-level controls and process controls that address those risks. This prevents teams from testing every process while missing a control that matters to reporting.

Create a deficiency log early, even before formal testing begins. Each entry should state the control gap, affected account, risk, owner, fix, due date, and retest result. Rate issues using an agreed framework and report open items on a set cadence. A log turns findings into owned work instead of unresolved audit discussion.

For a middle-market company, useful milestones are plain: complete the scope, document controls, test design, test operation, fix gaps, and retest. Add audit committee briefings at each key stage. This gives management time to improve controls before filing work tightens. It also creates an evidence trail the auditors and board can follow.

Need a second set of eyes before filing pressure builds? Talk to GuzmanGray about IPO readiness, controls, audit, and tax support.

Tax and entity structure items to resolve early

Tax and entity issues should be resolved early because they affect disclosures, diligence, audit support, and post-IPO compliance. CFOs should organize provision workpapers, entity charts, state filings, uncertain tax positions, equity records, and ownership documents before the transaction calendar tightens.

Tax provision readiness

An IPO readiness audit checklist should test the tax close before filing work crowds the calendar. Start with who owns the tax provision, which records feed it, and how each review step is shown. The goal is a repeatable process that produces support without a last-minute search.

Build a file for current and deferred tax items, key rate inputs, return-to-provision items, and review signoffs. Keep a separate list of uncertain tax positions, with the facts and approval for each view. If support is missing, assign an owner and due date now.

This work is not limited to federal income tax. Map state filing duties, sales and payroll tax issues, nexus questions, and any non-U.S. activity. A legal entity chart should match tax records, financial records, contracts, and board records. Differences may show work that must be cleared before drafting speeds up.

Equity and transaction choices

Equity awards need a tax review from grant through exercise, vesting, or settlement. Collect plan documents, award terms, value support, payroll treatment, and withholding records. Then flag unusual terms, cross-border workers, or missing approvals for focused review.

Transaction structure can also change the tax workstream. A conversion, reorganization, acquisition, or pre-IPO cleanup may affect ownership, attributes, or support needs. Tax, legal, accounting, and deal advisers should compare planned steps before they become hard to reverse.

- Confirm the entity chart and ownership history agree across teams.

- List open positions by tax type, location, period, owner, and support needed.

- Review equity award data against payroll, cap table, and approval records.

- Record the tax questions created by any planned transaction steps.

Why timing matters

Leaving tax until a registration statement is near completion creates avoidable pressure. The team may still trace records while counsel and auditors need clear answers. Early review gives management time to fix process gaps, gather evidence, and decide how open issues will be handled.

Use a tax readiness tracker with an owner, evidence request, status, due date, and reviewer for each item. Update it as entity or offering plans change. Tax then becomes an active part of readiness, not a late obstacle found during filing preparation.

What is a realistic IPO readiness timeline?

A realistic IPO readiness timeline starts months before filing work begins. CFOs should sequence close improvements, audit support, controls, tax positions, governance reviews, and adviser decisions so management can fix gaps before underwriters, auditors, and regulators require answers.

An IPO readiness audit checklist should begin before filing work sets the pace. For a CFO, the timeline is a sequence of proof: close quality, controls, audit support, tax positions, and coordinated decisions. It is not a promised listing date.

The right pace depends on current records, staff capacity, transaction history, and open issues. The SEC notes that companies should be flexible with their timetable, since market trends are hard to forecast. Plan by workstream and gate, then adjust when facts change.

Start with the gaps

The first phase should answer a direct question: what would fail review today? Map reporting gaps, audit adjustments, key controls, tax exposures, and missing support. This gives management a work plan, a budget view, and a sound basis for advisor discussions.

Run the initial gap assessment. Compare current reporting, governance, and staffing against public-company demands. Rank findings by filing risk and time to fix, not by ease.

Repair accounting records. Address close delays, account support, technical accounting memos, and complex transactions. Retain clean evidence for decisions, adjustments, and review sign-offs.

Build and test controls. Document who prepares, reviews, approves, and retains evidence for key processes. The SEC’s IPO building blocks stress reliable accounting controls and reporting systems.

Prepare for the audit. Set the audit scope, support list, data room rules, and issue calendar. GuzmanGray is a PCAOB audit requirements for IPOs authorized to audit public companies.

Review tax positions. Gather returns, provision workpapers, ownership history, uncertain positions, and state tax matters. Resolve documentation gaps before filing deadlines add pressure.

Coordinate the advisor team. Align auditors, counsel, tax advisors, underwriters, and management on owners and dependencies. Use one issue log with due dates and evidence status.

Confirm final readiness. Recheck open findings, financial statement support, control evidence, audit status, and filing inputs. Management should know every unresolved item and its response plan.

Build time for remediation

These steps often overlap, but they should not be rushed into a single sprint. A late accounting change can affect audit evidence, taxes, controls, and draft disclosures. A staffing gap can also slow reviews, even when records are sound.

Use milestone gates rather than an assumed launch month. For example, do not treat audit preparation as complete while major account support is still missing. If an issue changes the financial story, allow time for review and clear records.

The final readiness gate

Before filing activity accelerates, the CFO should have a current issues list and named owners. The team also needs support that can be retrieved without delay. A realistic timeline leaves room for questions, corrections, and market changes while keeping required work moving.

Which IPO readiness red flags should CFOs fix first?

CFOs should fix red flags that threaten reliable reporting first: late closes, unsupported estimates, revenue recognition gaps, equity record issues, tax provision weaknesses, missing committee evidence, and single-person dependencies. These problems can delay audit work and weaken public-company reporting readiness.

An IPO readiness audit checklist should begin with failures that can delay reliable reporting. A close that runs late, changes without support, or depends on one person deserves immediate attention. Public companies face annual, quarterly, and current reporting duties under SEC reporting requirements.

Close and estimate breakdowns

Start with the monthly close because every later workstream relies on it. Track open reconciliations, late journal entries, missing review signoffs, and accounts with unexplained swings. For material estimates, retain the model, source data, assumptions, reviewer approval, and updates after each reporting period.

Revenue recognition gaps move near the front of the queue as well. CFOs should compare contract terms to accounting conclusions. They should then test whether billing, delivery, credits, and deferred revenue follow the stated policy. A difference here can spread into forecasts and disclosures.

Do not rank issues only by account balance. A small, repeated close error can point to a broader review gap. Keep an issue log that records the cause, fix, evidence, reviewer, and whether the correction worked in the next close.

Equity, tax, and governance records

Next, clean up equity records and the tax provision file. Confirm approved grants, exercised awards, cap table ties, share-based compensation entries, tax calculations, and review evidence. Weak files create avoidable questions when auditors and counsel need a clear history.

Governance can be a quieter red flag. If audit committee reporting is not yet routine, set a calendar and a standard package. Include key estimates, close issues, control findings, and unresolved judgments. Reports from public companies generally include operations, financial condition, and management.

Named owners and advisor escalation

A readiness plan fails when a problem belongs to everyone and no one. Give each issue one company owner, a due date, proof, and a named advisor for escalation. Legal counsel can own filing questions; finance can own close fixes. Tax advisors can own provision gaps; auditors can review audit proof.

CFOs should also confirm that the audit firm fits the planned path to market. GuzmanGray states that it is a PCAOB-registered audit firm. That qualification does not replace clean records, but it shows who can support public-company audit work.

Use a simple triage rule: fix issues that block reliable reporting first, then clear gaps that slow review. Late closes, weak estimates, revenue conclusions, equity records, tax files, and missing committee reports should have owners before drafting begins.

Frequently Asked Questions

How long does an IPO readiness audit take for a middle-market company?

An IPO readiness audit should begin well before a planned offering date. An entire IPO can take 12 to 18 months, according to RSM. Timing depends on reporting gaps, transaction history, controls, staffing, and filing plans. Starting early gives CFOs time to document controls, resolve audit issues, select an appropriate auditor, and prepare financial statements for public-company scrutiny.

What should a CFO include in an IPO readiness audit checklist?

A CFO’s IPO readiness audit checklist should cover audited financial statements, close procedures, internal controls, tax exposures, governance, disclosure processes, auditor independence, and staffing. It should also identify owners and due dates for each gap. The SEC advises companies to assess accounting controls, reporting, and record-keeping systems for timely, accurate disclosure and compliance.

Does a company need a PCAOB-registered auditor before an IPO?

For a public-company audit, a CFO should engage an audit firm qualified to audit issuers under PCAOB requirements. Confirm the firm’s registration, independence, public-company experience, capacity, and approach to required communications before the filing process intensifies. GuzmanGray is a PCAOB-registered audit firm that can support public-company audit work. Early confirmation reduces the risk of an auditor transition during preparation.

How should CFOs budget for IPO readiness and ongoing public-company compliance?

CFOs should budget for both the transaction and the continuing cost of operating as a public company. Readiness spending can include audit and assurance work, tax reviews, controls remediation, reporting technology, governance support, legal counsel, and additional finance staff. The SEC recommends considering sufficient cash for the IPO process and the ongoing compliance costs of remaining public.

Ready to strengthen your IPO readiness plan?

Delaying an IPO readiness review can expose unresolved reporting, control, tax, or assurance questions when filing plans and stakeholder expectations become harder to adjust. Starting now gives CFOs more time to define required support, coordinate responsible teams, and resolve issues before an accelerated public-company audit timeline takes hold. That early work helps your advisors focus on planned decisions rather than avoidable last-minute requests during a high-pressure transaction period.

A focused discussion can help your team outline priorities, timing, responsibilities, and the support needed for the work ahead. Make decisions while preparation time remains, not after deadlines narrow your options. Ready to establish a clear path forward? Contact GuzmanGray for IPO readiness audit, assurance, tax, and advisory support.